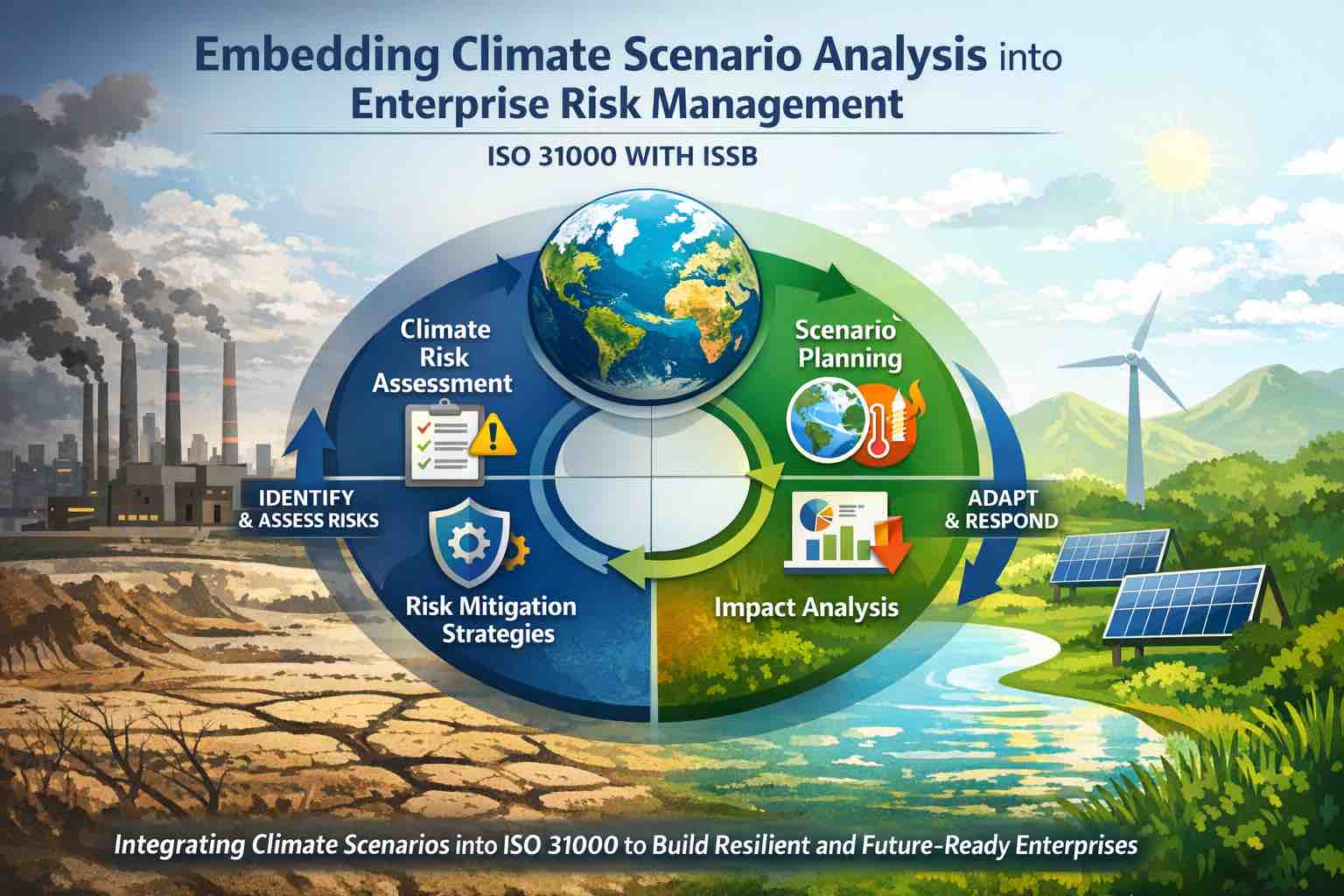

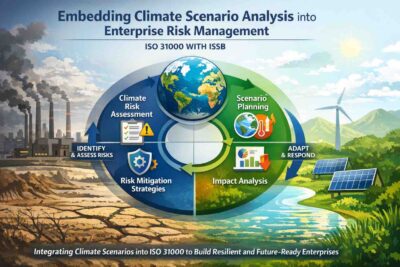

Embedding Climate Scenario Analysis into Enterprise Risk Management (ISO 31000 with ISSB)

Introduction: Climate Scenario Analysis as an ERM Discipline

A scenario is a coherent and plausible account of a future state of the world. Climate scenarios are not forecasts; rather, they are structured representations of how different climate pathways could unfold and how those pathways may affect economic systems, markets, and organisations.

As physical climate impacts intensify, market scenarios evolve, regulators and investors are placing increasing emphasis on climate-related disclosures. More importantly, boards are being challenged to demonstrate that climate considerations are embedded into the organisational strategy, risk posture, and capital allocation, rather than being treated as a parallel sustainability exercise. In fact, authorities are now directly linking climate scenario analysis to core risk governance expectations, as seen in the European Central Bank (ECB)’s 2022 climate stress test, where it observed that most banks were “not yet adequately prepared” to integrate climate risk into internal stress testing and risk management processes, despite widespread disclosure activity. The UK Prudential Regulation Authority (PRA) has also stated that climate risks should be treated as “financial risks” and they should be embedded within existing risk management frameworks.

As such, climate scenario analysis has evolved into a critical risk management lever. It enables organisations to examine how different climate futures could influence operating models, asset values, supply chains, and financial resilience. When applied rigorously, scenario analysis supports both qualitative judgement and quantitative assessment, allowing management to test strategic assumptions against uncertainty. In practice, however, climate scenarios often remain isolated within sustainability functions—disconnected from enterprise risk management (ERM) and many a time absent from board-level risk conversations.

This article sets out how climate scenario analysis can be embedded into ERM using ISO 31000 principles, and aligned with ISSB (IFRS S2) requirements—transforming climate analysis from a mere disclosure obligation into a governance and decision-making tool.

Types of Climate Scenarios

Climate scenarios model alternative pathways that might impact an organisation’s future business operations, such as the discharge of greenhouse gas emissions and the resulting temperature outcomes. These pathways shape the nature, timing, and severity of both physical and transition risks as the organisation scales and prepares itself for the future. The key scenarios are as follows:

Low-emissions scenarios aim to limit global warming to below 2°C.

They assume rapid policy intervention, accelerated decarbonisation, and technological change led by Management foresight and proactive decision-making. These scenarios typically involve higher near-term transition risk (as an organisation takes materially important steps) but deliver lower long-term physical impacts.

Intermediate-emissions scenarios

These reflect partial or uneven policy implementation. They sit between orderly but delayed transitions by organisations, and eventually produce mixed risk outcomes across regions and sectors.

High-emissions scenarios

These assume limited climate action and continuation of current operational practices. While transition pressures are lower initially, physical risks escalate significantly over time, affecting asset integrity, supply chains, and insurability. They also adversely impact an organisation’s long-term credibility and public image.

The above climate scenarios are already being leveraged by regulators. For instance, the Network for Greening the Financial System (NGFS) has developed reference climate scenarios which are now widely being used across central banks in Europe and Asia. These NGFS pathways underpin exercises conducted by the ECB, Banque de France, and several Asian regulators, as a market-led best practice in place of internally developed non-standard assumptions.

Purpose of Climate Scenario Analysis

The primary purpose of climate scenario analysis is to test the resilience of an organisation’s strategy under different plausible future outcomes. Rather than asking what is most likely to happen, scenario analysis models various possibilities—and whether the organisation is adequately prepared. By examining multiple pathways, organisations gain insight into how climate change could affect their potential future operations, assets, suppliers, customers, and financial performance. This supports stronger risk identification, more informed strategic choices, and better long-term planning.The importance of this discipline is well illustrated by past known failures, such as during the 2007–2008 financial crisis, where insufficient stress testing and narrow assumptions led to increased risk and eventually devastating economic outcomes. Scenario analysis exists to avoid such blind spots, through objectively challenging popular assumptions and subjecting them to various ‘what-if’ tests before adopting long-term strategies.

Why Climate Scenario Analysis Often Fails

Despite widespread adoption, many organisations struggle to extract decision value from climate scenario analysis. Common failure points include:

Poor risk classification: Climate risks are often discussed in broad narrative terms, without a clear distinction between physical, transition, liability, and opportunity dimensions. The ECB has observed that institutions find it difficult to translate climate risks into standardised risk categories such as credit, market, operational, and liquidity risk. Where climate risks remain framed only as high-level sustainability narratives, they fail to meet acceptable risk classification and are no longer part of Management conversations.

Misalignment with ERM processes: ERM frameworks require defined likelihood scales, impact metrics, and control assessments. Climate scenario outputs frequently sit outside these structures, produced by separate teams using different assumptions. As a result, climate risks fail to meet ISO 31000 standards and are excluded from enterprise risk registers.

Fragmented governance: Climate risk ownership is often delegated to sustainability or ESG working groups, while strategic and financial risks are centralised in alternate functions. This fragmentation creates accountability gaps and leads to climate insights rarely influencing risk prioritisation or strategic decisions.

Scenario Models: Understanding 1.5°C and 2°C Pathways

The distinction between 1.5°C and 2°C scenarios is not purely academic. These pathways represent different risk dynamics and management challenges.

1.5°C scenarios assume rapid and coordinated global action through a global acceptance of risk and rapid decision-making by influencers across marquee businesses. Emissions are assumed to decline sharply, reaching net zero around mid-century. For organisations, this creates:

- Accelerated transition risk through process and technological shifts.

- Shorter asset lifecycles and faster repricing by suppliers

- Increased exposure to policy, technology, and market shifts – that are often regulator-dictated

These scenarios are, however, relevant for testing strategic adaptability, capital deployment timing, and stranded asset risk.

2°C scenarios, on the other hand, allow for a more gradual transition. Emissions reductions are slower, and policy responses may be delayed. This results in:

- A more prolonged transition period for Management

- Rising physical risks over time

- Greater uncertainty around long-term asset resilience, but lower upfront costs

Boards should view both these scenarios as stress tests for operational continuity, supply chain resilience, and long-term financial exposure. Effective ERM does not select a ‘best-case’ scenario. Instead, it uses multiple pathways to define the boundaries of acceptable risk and guardrails future operations through a ‘blended approach’.

Translating Scenarios into Risk Registers

Embedding climate scenarios into ERM requires deploying methods to convert uncertainty into structured risk information. ISO 31000 defines risk as the effect of uncertainty on objectives—making it directly applicable to climate analysis.

A disciplined translation process includes:

- Establishing context: Define internal and external factors, time horizons, and strategic objectives affected by climate risk

- Risk identification: Translate operational outcomes into clear risk statements, specifying source, event, and impact

- Risk analysis: Assess likelihood, consequence, and materiality under each scenario, using consistent ERM scales

- Risk evaluation: Compare assessed risk levels against defined risk criteria and appetite thresholds

- Risk treatment: Identify mitigation, adaptation, transfer, or acceptance strategies aligned with ISO 31000

- Integration and monitoring: Climate risks must be embedded within existing ERM taxonomies—not maintained as standalone ESG categories

- Risk registers should be reviewed and updated as scenarios, assumptions, and exposures evolve.

In reality, authorities are increasingly assessing whether this translation has happened. In recent climate-focused reviews, firms have been challenged where scenario outputs could not be traced back to specific risk entries, owners, and mitigation actions within their ERM framework.

Aligning Climate Risk with Risk Appetite

Many organisations articulate climate ambitions but stop short of defining risk tolerance. Risk appetite alignment requires explicit choices.

Boards must determine:

- Which climate risks are acceptable, constrained, or avoided in the operational context

- Where exposure exceeds appetite under specific scenarios of the current and future business plan

- How climate risk interacts with financial thresholds and strategic objectives

Effective alignment involves:

- Defining quantitative and qualitative risk indicators

- Establishing thresholds linked to regulatory exposure, supply chain dependency, or asset concentration

- Differentiating between risk appetite and risk capacity

- Assigning clear accountability for breaches and escalation

Without this step, climate scenario analysis remains informative, but not objective enough to base Management decisions.

Board Oversight Structures: Moving Beyond ESG Committees

Climate risk frequently fails at the governance level, not due to a lack of data, but due to inadequate actionable oversight. When climate issues are handled by ESG committees while risk and investment decisions sit elsewhere, no single body owns climate risk end-to-end. As such, this fragmentation prevents climate insights from influencing rapid Management actions, operational decisions, capital allocation, long-term strategy, or risk tolerance.

Effective oversight embeds climate risk within:

- Board risk committees (risk exposure and appetite)

- Audit committees (financial impacts and controls)

- Full board deliberations (strategic resilience)

Climate risk should be governed as an enterprise risk, not a sustainability topic.

Disclosure vs Decision Use: The Core Tension

A fundamental challenge in climate scenario analysis is the gap between disclosure and decision use.

Disclosure communicates information, whilst decision-making directs action. When scenario analysis is conducted primarily for reporting, it becomes narrative-driven and retrospective in approach. However, when it is used for decision-making, it becomes forward-looking, financially grounded, and operationally relevant.

Closing this gap requires:

- Integrating scenario outputs into ERM and capital planning

- Linking analysis to defined risk appetite thresholds

- Using scenarios to inform real strategic choices

ISSB disclosures should reflect decisions already taken, but not substitute for them.

Integrating ISO 31000 and ISSB

ISO 31000 provides the process discipline for managing risk. ISSB IFRS S2 defines the expectation for climate resilience and disclosure. Together, they enable climate risk to be managed systematically and reported credibly.

When scenario analysis is embedded into ERM:

- Disclosures become consistent and auditable

- Governance responsibilities are clear

- Climate risk moves from narrative to enterprise intelligence

Conclusion

Embedding climate scenario analysis into ERM is not about improving reports. It is about creating long-term value by converting climate uncertainty into strategic insight.

When aligned with ISO 31000 and ISSB, scenario analysis strengthens governance, sharpens risk appetite, and enables more informed, forward-looking decision-making. Organisations that achieve this integration are better positioned not only to manage climate risk, but to navigate uncertainty with confidence and discipline.

CorpStage ESG 360 bridges climate scenarios with enterprise risk and financial decision-making—turning uncertainty into actionable strategy. It empowers organisations to embed ISSB-aligned, ISO 31000–driven risk intelligence into everyday business decisions.

Learn more about – audit readiness

Download the pdf here- Embedding Climate Scenario Analysis into Enterprise Risk Management

Visit for more: https://www.corpstage.academy/