Audit-Ready ESG Reporting: How to Build Assurance-Grade ESG Systems That Withstand Scrutiny

ESG assurance platform and audit-ready ESG systems That Withstand Scrutiny- Why ESG Reporting Is Now Treated Like Financial Reporting

ESG reporting has undergone a structural transformation. What was once a narrative-driven sustainability exercise has now evolved into a rigorous, evidence-based discipline aligned with financial reporting standards.

Global regulatory bodies such as the International Sustainability Standards Board, International Auditing and Assurance Standards Board, and European Securities and Markets Authority have collectively raised expectations around data quality, traceability, and assurance readiness.

Today, ESG disclosures are evaluated not just for what they say—but for:

- How the data is generated

- Whether controls exist and operate effectively

- If the information can withstand audit scrutiny

This shift is being reinforced by capital markets, where investors increasingly rely on ESG data to assess risk exposure, resilience, and long-term value creation.

What Auditors Actually Evaluate in ESG Reporting

A common misconception is that ESG audits focus on verifying numbers.

In reality, auditors focus on system integrity and process reliability.

They assess:

- The strength and origin of supporting evidence

- The effectiveness of internal controls

- The traceability of data across systems

- The consistency and repeatability of processes

Rather than recalculating ESG metrics, auditors test whether the systems producing those metrics are reliable and governed.

👉 This is where most organisations fail—by prioritising better numbers instead of better systems.

Evidence: The Core of Assurance-Ready ESG Reporting

In ESG assurance, evidence overrides narrative.

Auditors require objective, verifiable documentation to support every disclosure. This includes:

- Source-level data (e.g., meter readings, system logs)

- Calculation methodologies and assumptions

- Approval workflows and control checkpoints

- Version histories and audit trails

The Financial Reporting Council has repeatedly highlighted that organisations struggle not due to lack of documentation—but due to inability to explain, justify, and trace that documentation.

Typical Failure Scenario

A company discloses Scope 3 emissions with detailed methodology—but cannot demonstrate:

- When the methodology was approved

- Who validated it

- How it has evolved over time

- What source data supports it

👉 Without this, disclosures fail assurance—even if the numbers appear reasonable.

ESG Internal Controls: Applying Financial Discipline to Sustainability Data

To achieve audit-ready ESG reporting, organisations must implement robust internal control frameworks, similar to those under the Sarbanes-Oxley Act.

Three Critical Types of ESG Controls

1. Preventive Controls

- System validation rules

- Locked emission factors

- Standardised methodologies

2. Detective Controls

- Variance analysis

- Trend monitoring

- Exception reporting

3. Review Controls

- Independent validation processes

- Maker-checker workflows

- Documented approvals

However, regulators like ESMA have observed a consistent issue:

👉 Controls are often designed—but not executed or evidenced in practice.

From an auditor’s perspective, a control without evidence is equivalent to no control.

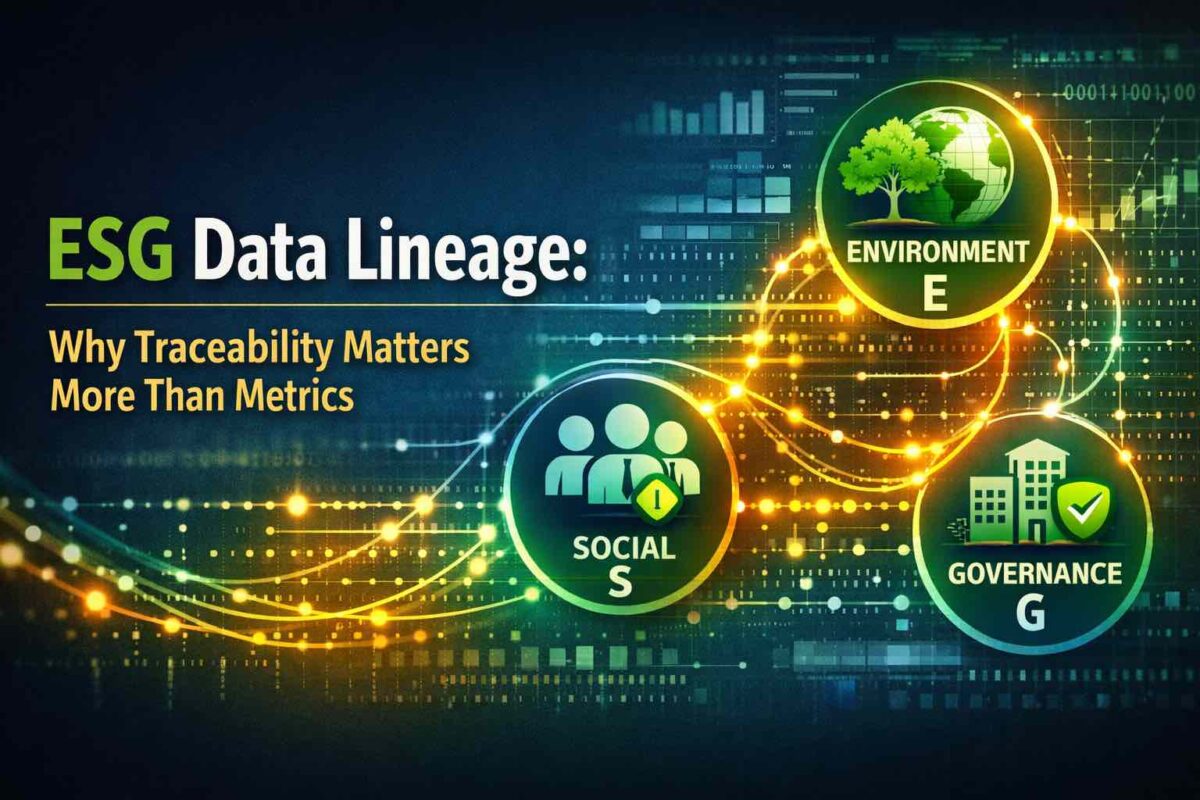

Traceability: The First Test of ESG Data Credibility

Traceability is typically the first and most critical test performed during ESG assurance.

Auditors attempt to:

- Trace final disclosures back to source-level data

- Validate each transformation step in the data flow

- Confirm version control and calculation logic

The International Organization of Securities Commissions has reinforced that traceability is essential to build investor trust and market confidence.

The Core Risk

Many organisations rely on:

- Manual spreadsheets

- Offline data aggregation

- Uncontrolled transformations

This creates a fundamental problem:

👉 If ESG data cannot be traced end-to-end, it cannot be assured.

How Auditors Test ESG Data: The Role of Sampling

Auditors do not review entire datasets—they rely on sampling methodologies.

Sampling is influenced by:

- Materiality of ESG metrics

- Complexity of estimation models

- Historical error patterns

For example:

- Scope 1 and fuel data → smaller samples

- Scope 3 emissions → larger, more detailed samples

Insights from the European Central Bank suggest that higher uncertainty leads to deeper scrutiny.

👉 Key takeaway:

Improving a few reported numbers does not improve audit outcomes.

Improving systems and controls does.

The Spreadsheet Problem: Why Most ESG Systems Fail

One of the most persistent weaknesses in ESG reporting is overreliance on spreadsheets.

Key risks include:

- Lack of structured data models

- No audit trails

- High manual error probability

- Easy override of controls

The Financial Stability Board has identified spreadsheet-driven reporting as a major source of data aggregation risk.

What Organisations Should Do Instead

- Implement centralised ESG data platforms

- Build automated data pipelines

- Apply role-based access controls

- Ensure system-generated audit trails

Spreadsheets may still be used—but only for limited input purposes, not as the core system.

When ESG Systems Fail: Lessons from Real-World Cases

Failures in ESG systems often lead to reputational and financial consequences.

- Volkswagen Group highlighted governance and data integrity failures

- Shell plc faced investor pressure over misalignment between disclosures and underlying data

These cases demonstrate a critical truth:

👉 ESG failure is rarely about disclosure—it is about credibility of systems and controls.

Common ESG Reporting Failure Points

Organisations aiming for assurance readiness should watch for:

- Evidence created after the fact, not during processes

- Controls that are assumed but not tested

- Fragmented systems across departments

- Excessive reliance on manual processes

- Weak governance and unclear ownership

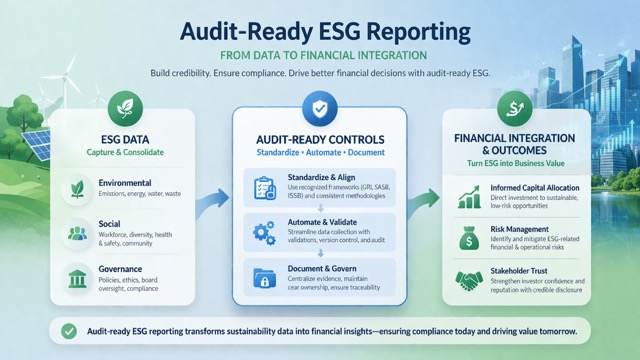

What Audit-Ready ESG Reporting Actually Looks Like

An organisation prepared for ESG assurance will demonstrate:

✔ Structured, complete, and verifiable evidence

✔ Clearly defined and operational internal controls

✔ End-to-end data traceability

✔ Consistent methodologies across reporting periods

✔ Integrated systems with audit-ready workflows

Importantly:

Audit readiness is not achieved by adding documentation—it is achieved by designing systems that generate evidence by default.

Conclusion: ESG Credibility Is Built on Systems, Not Narratives

The future of ESG reporting lies in credibility, not communication.

Organisations that succeed will be those that:

- Build evidence-first ESG systems

- Embed controls into processes

- Ensure traceability by design

- Align ESG with financial reporting discipline

👉 In today’s capital markets, ESG reporting is no longer judged by intent—but by proof.

How CorpStage Enables Audit-Ready ESG Reporting

Most organisations today recognise the importance of audit-ready ESG reporting, but struggle to operationalise it across systems, controls, and governance.

This is where CorpStage ESG 360 is designed to deliver measurable value.

CorpStage goes beyond traditional ESG tools by enabling organisations to build assurance-grade ESG systems that integrate directly with financial processes.

1. Build Evidence-First ESG Data Architecture

CorpStage ESG 360 establishes a structured ESG data environment across the organisation:

- Integration with ERP, HRMS, IoT, and supplier systems

- Centralised ESG data repository with end-to-end traceability

- Automated data ingestion pipelines for Scope 1, 2, and 3 emissions

👉 Every ESG metric is linked back to source-level evidence, ensuring audit readiness by design.

2. Embed Internal Controls into ESG Processes

CorpStage enables organisations to implement financial-grade internal controls for ESG data:

- Maker-checker workflows and multi-level approvals

- Preventive and detective control mechanisms

- Locked methodologies and version-controlled calculations

👉 ESG data is governed with the same discipline as financial reporting.

3. Ensure Complete Data Lineage and Traceability

Audit success depends on traceability—and CorpStage is built around it:

- Full audit trails across data lifecycle

- Version history and change logs

- Drill-down capability from disclosure → calculation → source

👉 This allows organisations to defend ESG disclosures under audit scrutiny with confidence.

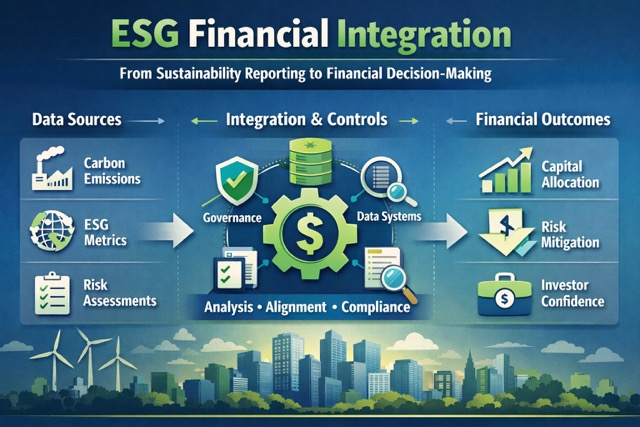

4. Align ESG with Financial Decision-Making

CorpStage bridges the critical gap between sustainability and finance:

- Integration of ESG metrics into financial planning and capital allocation

- Climate scenario analysis linked to financial outcomes

- Risk and opportunity mapping with quantified financial impact

👉 ESG moves from reporting to strategic decision-making capability.

5. Achieve Assurance Readiness Faster

CorpStage accelerates the journey to ESG assurance readiness:

- Pre-built templates aligned with ISSB S1, S2, CSRD, and GRI

- Evidence management systems for audit support

- Mock audit workflows and readiness diagnostics

👉 Organisations are not just compliant—they are audit-prepared and investor-ready.

From ESG Reporting to ESG Credibility

The future of ESG is not about producing more reports—it is about building systems that withstand scrutiny.

With CorpStage, organisations can:

✔ Transition from fragmented ESG data to integrated systems

✔ Move from narrative disclosures to evidence-based reporting

✔ Strengthen investor confidence through assurance-ready ESG processes

Start Your ESG Transformation Journey

If your organisation is preparing for ISSB, CSRD, or ESG assurance requirements, the time to act is now.

👉 Explore how CorpStage ESG 360 can help you build audit-ready ESG systems that connect sustainability with financial performance.