ISSB S1 and S2 Implementation Guide: Moving from ESG Reporting to Financial Integration

ESG Financial Integration- Why ISSB Standards Are Reshaping ESG Reporting in Capital Markets

The introduction of ISSB IFRS S1 and IFRS S2 standards marks a decisive shift in how organisations approach sustainability reporting. These standards are not designed to increase reporting burden—they are intended to embed sustainability into financial decision-making, risk management, and capital allocation.

Backed by global regulators such as the International Organization of Securities Commissions, ISSB standards have elevated ESG disclosures from narrative reporting to investor-grade financial information.

Today, sustainability data is no longer peripheral—it directly influences valuation, cost of capital, and investor confidence.

The Core Problem: Why Most ISSB Implementations Fail

Despite widespread adoption efforts, most organisations are still misinterpreting ISSB S1 and S2.

Instead of treating them as enterprise-wide system requirements, companies often approach them as:

- Disclosure checklists

- Sustainability team outputs

- Standalone reporting exercises

This leads to a fundamental breakdown:

- ESG teams operate independently

- Finance teams remain disconnected

- Risk and strategy functions are not integrated

The result?

High-quality reports with low credibility under investor or audit scrutiny.

ISSB S1 vs S2: What Actually Changes in Practice

Understanding the distinction between S1 and S2 is critical for effective implementation.

IFRS S1 – Enterprise-Wide Sustainability Integration

- Covers all sustainability-related risks and opportunities

- Establishes linkage between ESG and business value

- Requires integration across governance, risk, and strategy

- Focuses on enterprise-level data architecture

IFRS S2 – Climate-Specific Financial Impact

- Focuses specifically on climate-related risks and opportunities

- Requires scenario analysis, emissions data, and transition plans

- Emphasises financial materiality of climate risks

- Has higher assurance expectations (modelling, assumptions, estimates)

Where Companies Go Wrong

Most organisations:

- Over-invest in climate modelling (S2)

- Under-invest in governance and systems (S1)

This creates a dangerous imbalance:

Advanced climate scenarios without credible data governance or controls.

The Financial Integration Gap: Where ESG Systems Break Down

The biggest failure point in ISSB implementation is financial integration.

Evidence from the European Central Bank revealed that many institutions could not:

- Link climate risks to balance sheets

- Integrate ESG assumptions into financial planning

- Translate sustainability risks into cash flow impacts

This pattern is now visible across industries:

- Climate risks identified, but not reflected in budgets

- Scenario analysis conducted, but not used in decision-making

- Emissions data collected, but not linked to capital allocation

A well-known example is Shell plc, where investor scrutiny highlighted the gap between net-zero commitments and capital expenditure decisions.

This is precisely the gap ISSB aims to close:

From disclosure → to decision-making

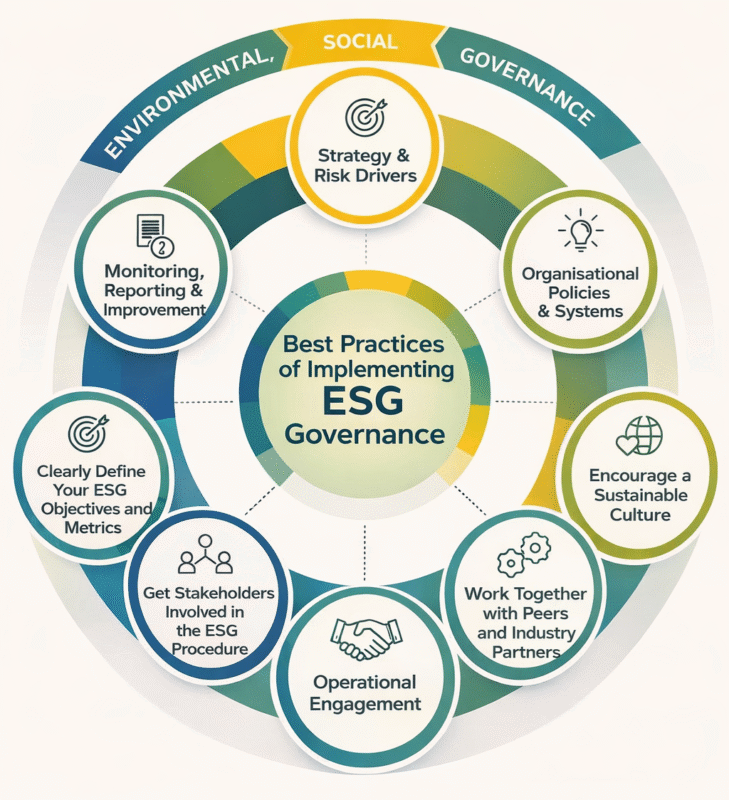

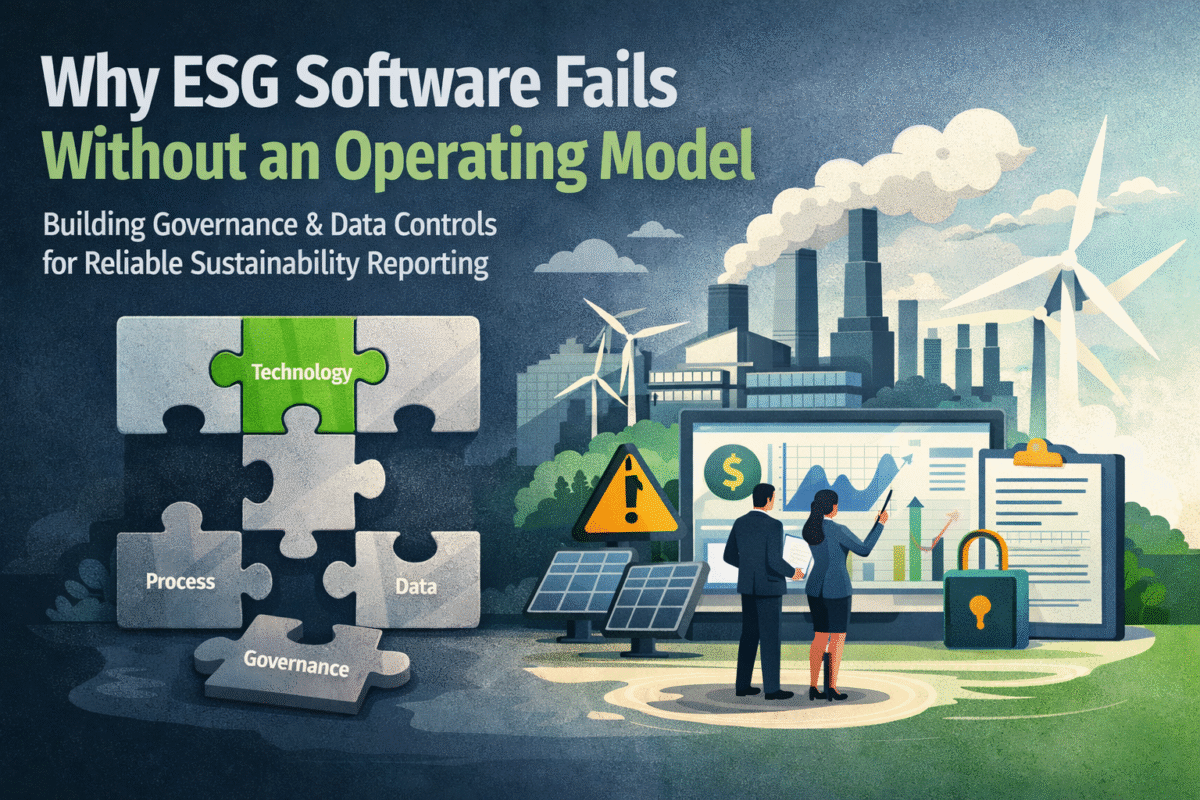

Governance: The Foundation of ISSB Compliance

ISSB implementation is not a data problem—it is a governance problem first.

The Financial Reporting Council has repeatedly identified weak governance as the primary reason ESG disclosures fail under scrutiny.

Common Governance Failures

- ESG committees operating in isolation

- Lack of ownership between finance and sustainability teams

- Absence of documented controls and accountability

- Weak board-level oversight

What Good Governance Looks Like

Leading organisations such as Unilever demonstrate:

- Board-level ESG integration

- Alignment between sustainability strategy and financial decisions

- Clear accountability across functions

ISSB success requires integration across board, audit, risk, and executive functions.

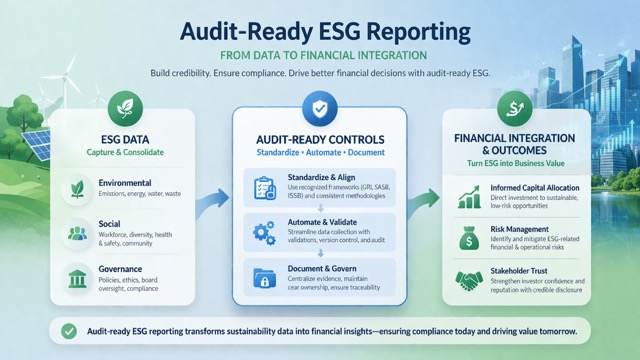

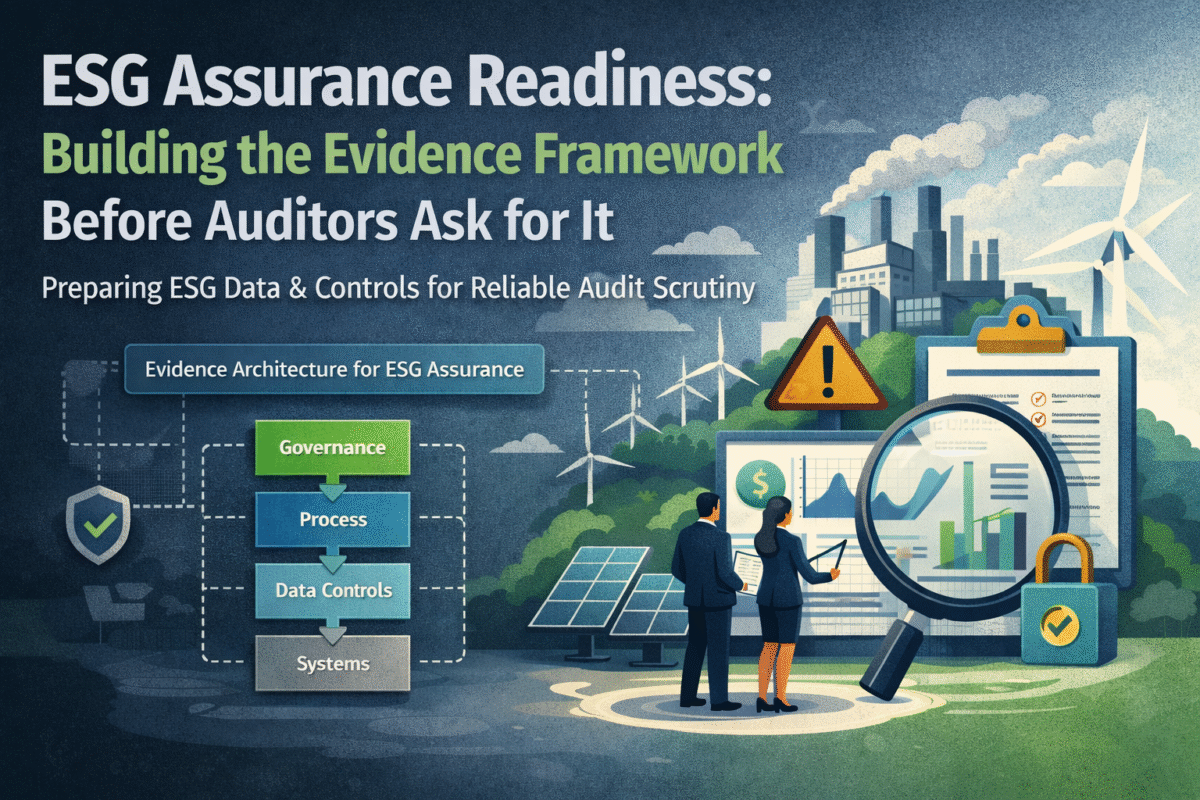

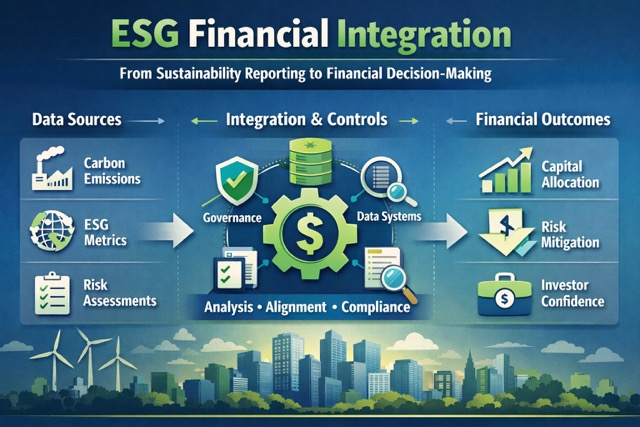

ESG Data Architecture: The Hidden Constraint

A major barrier to ISSB implementation lies in weak ESG data systems.

The European Securities and Markets Authority has flagged inconsistent ESG disclosures due to:

- Poor data traceability

- Lack of system integration

- Weak control environments

The ISSB-Aligned Data Architecture Model

To achieve assurance-ready ESG reporting, organisations must build a three-layer architecture:

1. Source Layer (Data Capture)

- ERP, HRMS, energy systems

- Supplier data (Scope 3 emissions)

- Climate models and external inputs

2. Control Layer (Validation & Governance)

- Calculation methodologies

- Approval workflows

- Version control and audit trails

3. Disclosure Layer (Reporting Output)

- Direct mapping to ISSB S1 & S2

- Read-only outputs

- Prevention of last-minute manipulation

Companies that calculate ESG metrics only at the reporting stage will fail assurance due to lack of data lineage and control traceability.

Internal Controls: Applying Financial Discipline to ESG

ISSB introduces a fundamental expectation:

ESG data must be governed with the same rigour as financial data.

This aligns closely with principles under the Sarbanes-Oxley Act.

Key Control Types for ESG Systems

Preventive Controls

- System validations

- Mandatory fields

- Locked methodologies

Detective Controls

- Variance analysis

- Reconciliations

- Trend monitoring

Governance Controls

- Maker-checker workflows

- Role-based approvals

- Evidence documentation

The reality:

Most organisations define controls but fail to operationalise them.

Assurance Readiness: Designing ESG Systems for Audit

ISSB assumes that ESG disclosures will be subject to assurance.

This means organisations must be able to demonstrate:

- Data lineage from source to disclosure

- Consistency in methodologies

- Evidence of control execution

Companies like Volkswagen Group have strengthened their ESG systems to meet assurance expectations.

Critical insight:

Assurance failures rarely arise from incorrect numbers—they arise from weak systems, processes, and governance.

How to Implement ISSB S1 & S2: A Practical Framework

A structured implementation approach typically involves five phases:

Phase 1: ESG Diagnostic & Gap Assessment

- Identify gaps across governance, data, and controls

- Map current state vs ISSB requirements

Phase 2: Define Boundaries & Methodologies

- Standardise calculation methods

- Establish organisational boundaries

Phase 3: Build ESG Data Architecture

- Integrate systems across departments

- Implement control frameworks

Phase 4: Achieve Assurance Readiness

- Document processes

- Conduct internal testing and mock audits

Phase 5: Continuous Improvement

- Refine methodologies

- Improve data quality and system maturity

Why ISSB Matters: The Capital Markets Perspective

ISSB is fundamentally about capital markets trust.

Investors increasingly rely on ESG data to assess:

- Transition risks

- Long-term cash flows

- Strategic resilience

Organisations that fail to implement ISSB effectively face:

- Reduced investor confidence

- Higher cost of capital

- Increased scrutiny from regulators

Conclusion: From ESG Reporting to ESG Credibility

ISSB S1 and S2 are not just reporting standards—they represent a new operating model for ESG.

They require organisations to move:

- From narrative → to measurable data

- From sustainability → to financial integration

- From compliance → to strategic decision-making

Ultimately, companies that succeed will be those that:

✔ Integrate ESG into financial systems

✔ Build governance-led ESG architectures

✔ Deliver assurance-ready disclosures

This is where ESG transitions from a reporting exercise to a driver of enterprise value and capital allocation discipline.